Rapid Refund

Jump the queue, get 50% paid upfront

Average Claim £3,000

We'll tell you straight away what you're owed

Free to enquire

It's free to find out if you have a claim

No Hidden Costs

All aftercare is included

We've collected the answers to the most common questions we get here. If your question isn't answered, or if you just prefer to talk to a real person right away, you can give us ring, use the Live Chat here on our site, join us on Facebook or send us a message for help.

Most likely, yes. The amounts you receive don’t normally cover everything you’re entitled to.

It is important to know that we deduct HDT or GYH allowances from any claim we make as both are paid non-taxed.

Use our Tax Refund Calculator to find out if you are owed anything from HMRC

If you live in married quarters, on or off base, and spend your leave periods there, it would normally be classed as your main residence. The claim in this case would be for any costs for travel between your married quarters and any temporary postings of up to 24 months.

If you already receive a Home to Duty (HDT) allowance for this already, we will review the amounts received against the allowable limits and claim for any shortfall.

Use our Tax Calculator to see if you are owed a refund from HMRC.

If you live on base part of the time but go home to another address for weekends or longer periods of leave, the leave address would be classed as your main residence.

A tax refund claim in this case would be for travel between your home address and your workplace.

If you already receive a Get You Home Travel (GYH) allowance for this, we will review the amounts received against the allowable limits and claim for any shortfall.

Use our Tax Calculator to find out if you are due a refund.

Yes this is very important as we need to have documentary evidence to support your claim.

Please ensure you keep a copy of each of your Assignment Orders for each base that you have traveled to. You can print these from JPA but please note these are deleted after 60 days.

See our checklist of the documents you will need to make a claim. We can help you get copies of anything you are missing if needed.

It will depend on the type of training.

HMRC has strict rules about what is classed as an allowable expense around training. If it was an essential part of your contractual duties of employment then we might be able to claim for the traveling expense or mileage.

You will need to have completed your phase one training to make a claim.

Even if you not due a refund this year remember that you can claim for the past 4 tax years so use our tax calculator to find out if you are owed anything.

To get a tax refund, HMRC says you need to be travelling to temporary workplaces. Reservists and Territorial Army personnel tend to spend most of their service in one place, which wouldn't qualify and is an example of when you wouldn't be able to claim an MOD tax refund.

That said, your circumstances might be different from most. Get in touch if you want us to look into it for you. It costs you nothing to find out where you stand.

Use our tax calculator to see if you are due a refund

Find out if you need to complete a Self Assessment Tax Return or if you can claim Flat Rate Expenses.

Yes. You are legally entitled to reclaim 24p per mile, which is the difference between the HMRC allowed rate of £0.45 per mile* and the MOD £0.21 per mile tax exempt allowance. To claim this, you must be on temporary duty. This is defined by the relevant HMRC legislation, not by MOD policy.

HMRC mileage refunds explained

Ask RIFT about your specific circumstances if you are still unclear.

*HMRC EIM32080 Travel expenses: travel for necessary attendance: temporary workplace: limited duration, the 24 month rule.

Despite what some people are saying, MOD personnel really can get UK tax refunds. RIFT Refunds always knew this was true and we fought hard to get the proof. You can read the MOD letter to us and feel assured that this is something that can be legitimately claimed for.

Tax refunds for travel can be claimed, as confirmed in DIN ‘2015DIN01-005’ which has been issued to all service personnel to officially confirm this.

There has been a lot of confusion around tax refunds that RIFT has worked hard to clear up with both the MOD and HMRC.

Different interpretations of what is meant by ‘a temporary posting’ have caused this confusion. Some believed that individuals who claimed a tax refund on HDT were doing so in breach of HMRC rules. RIFT can categorically confirm that none of these potential situations can arise and this is confirmed by the MOD.

Some also thought that making any claim for a tax refund may mean the individual may have to repay rebated money in the future. Others also thought claiming a refund would jeopardise the whole tax exemption of the MOD HDT allowance, disadvantaging many service personnel.

Others were worried about changes to tax codes. Your tax code should not change due to a refund claim but any problems with your tax code are covered in our aftercare service which means we will get any errors fixed for you at no extra charge. Read more about tax codes and how to check if yours is correct.

DIN ‘2015DIN01-005’ has been issued to all service personnel to officially confirm that tax refunds for travel are claimable.

It also states that you can use an agent to make a claim for you. RIFT will act as your agent, providing an end to end service if you don’t have the time or are not comfortable dealing with the technical legislation set out by HMRC.

This supports the previous formal confirmation we received from the Ministry of Defence.

Just like anyone else, you're entitled to a UK tax refund for travel expenses to and from temporary workplaces. If you're making your own way from a UK residence, you could have a pretty big refund on your hands. Watch out, though - if your family has moved abroad with you, then your main residence might be outside the UK. In that case, you can't claim for your travel costs.

Find out everything you need to know about paying UK tax if you work overseas or get in touch.

Yes, if this is classed as your main residence.

The legislation for tax refund claims is based on costs for travel expenses on to temporary postings of under 24 months, even outside the UK, using either your own vehicle or public transport counts.

If you're in the Armed Forces and making your own way to more than one base, you can claim any overpaid tax on the cost of that travel for the last 4 years, and the RIFT average 4 year rebate is £2,500.

HMRC takes a big enough bite out of your pay already. Don't let them hold onto cash that's supposed to be in your pocket. Use our tax calculator to find out if you are owed anything back.

No, laundry costs are included in your annual personal allowance (i.e. the amount you can earn tax-free each year). This will be recorded in your tax code.

You may be able to claim if you have the receipt and it is in the last four tax years as it is a work related expense.

Use our tax calculator to find out if you are due a refund.

Yes, the cost of flying varies considerably so we need evidence of your actual expenses for HMRC. We can only claim for the actual flights you made, not the cost of any flights between two destinations.

Have a look at our checklist of the documents or paperwork we'll need for your claim.

You can download all your wage slips from the JPAC website.

Under HMRC legislation a posting that is more than 24 months is deemed permanent and therefore the temporary workplace rules don’t apply. However, we would review every case in isolation as we would need to understand your expectation at the outset of your posting.

As you can claim for the previous 4 years even if you have been at your current base for over 24 months you may be able to claim for previous postings.

Use our Tax Calculator to work out if you are due a refund.

We need the following information to assess your MOD tax refund and then hopefully process your claim:

See our full document checklist and what to do if you are missing anything.

Other information – We’ll ask you a few simple questions about your financial circumstances e.g. if you have any other sources of income such as rental income, whether you have a student loan or a private pension that may affect your claim, your tax code or mean that you need to submit a self assessment tax return.

The MOD accommodation rules may also have an impact so we will need to understand your living arrangements. This helps us calculate the value of tax you’ve overpaid.

Use our Tax Calculator to find out if you are due money back.

Armed Forces uniform tax rebates are handled differently from most other professions. Generally speaking, your uniform maintenance costs are handled through your tax code. Basically, your tax-free Personal Allowance gets ratcheted up a few notches to make up for what you're shelling out.

The taxman likes to be kept up to date on any income you’re earning, but he’s not some crazed stalker prying into every aspect of your private life. Gifts from your parents or friends, student loans and grants don’t count as taxable income in HMRC’s eyes. The same goes for bursaries, scholarships and so on.

Yes. If you’re renting out a room while you’re studying, then the taxman will want his bite of it. As always, any Personal Allowance you’re entitled to applies. You’ll probably end up filing Self Assessment tax returns to account for the income. However, depending on what you’re renting out, you might be able to use the Rent a Room scheme. Under Rent a Room, you can earn up to £7,500 tax-free a year from renting out furnished accommodation in your main home. Rent a Room is simpler for most people than working out their expenses in their tax returns. As long as you qualify for it, it can be a decent way to score some extra income.

Visit our guide to tax on rental income.

Apprenticeships are a lot like training contracts, in that you’re working primarily to learn a trade or set of skills. However, apprenticeships are paid positions. That means you’ll be taxed through the PAYE system. Depending on how long your apprenticeship lasts, you might find yourself claiming back some PAYE tax from HMRC (if it’s less than a full year, for instance). Also, unless your employer’s paying or reimbursing all your expenses (travel to temporary workplaces, tool/equipment repair, and so on), you might be owed some tax back for those, too.

Tax breaks are another term for tax relief. HMRC has various systems in place to help people and businesses bring down the tax they're paying under certain circumstances. For example, when you're reaching into your own pocket for things like travel to temporary workplaces, you can claim back some tax on your mileage expenses. Everything from individuals washing their work uniforms to businesses conducting cutting-edge R&D can qualify for some kind of tax relief. The key to getting the best from these systems is to know exactly what you qualify for, and how to claim it back.

If you're self-employed and paid through the Construction Industry Scheme (CIS), you're probably due a tax refund.

You can also claim back a range of job-related expenses, including travel, meals, lodging, parking, tolls, tools, protective clothing, public liability insurance, phone bills, postage and stationery.

We’ll assess all your expenses and include them if they qualify. That way you'll be certain that everything on your claim is a genuinely allowable expense and you won't find HMRC knocking on your door asking for their money back. If you're a RIFT customer, you'll be covered by our RIFT Guarantee as well, so you've got even more peace of mind.

Sadly there are a number of unscrupulous tax refund advisors taking advantage of CIS workers at the moment.

If you want to see how much you could be due back from HMRC use our CIS Tax Calculator and find out in seconds.

Find out more about the Construction Industry Scheme (CIS) and how to register if you need to.

Read our guide to CIS and Self-Assessment

Yes it does. All self-employed people, including CIS workers, have to complete a tax return every year. The tax year ends on 5th April and you’ve got until 31st January the following year to send your tax return to HMRC.

Read more about Tax and the Construction Industry Scheme

At RIFT we complete your tax return for you, and claim your tax refund at the same time. Just tell us where you’ve worked, and when, and we’ll work out the cost of your travel. We’ll add any other job-related expenses you may have and fill in the tax forms for you, all you need to do is sign them.

We’ll send the forms to HMRC, handle any questions on your behalf and chase them if they don’t pay out in the agreed timescale – it’s all part of our service.

95% of our CIS customers get a tax refund, and the average value of the refunds is £1,705 per year.

Read our guide to CIS and Self-Assessment

Use our CIS tax calculator to find out how much you could have waiting for you at HMRC.

CIS tax rebates generally take about 4-10 weeks for HMRC to process. RIFT’s CIS refund service includes handling your Self Assessment CIS tax return and full aftercare throughout the year, with no hidden prices. With RIFT, you get the very best from your claim, as fast as possible and with no expensive hourly rates to cough up. One simple fee takes care of everything.

HMRC’s not known for its blistering speed, but there are a few things you can do to keep the wheels turning on your claim:

RIFT’s expert teams will make sure there's no hold-up at HMRC. That means no endless waits on HMRC helplines and no dangerous mistakes creeping into your claim. We'll even chase up old employers if they're dragging their feet in sending the information we need. Once you’re happy with the amount we’ve calculated for your rebate, we’ll chase up HMRC until it’s paid out in full. Meanwhile, we take expert care of you all year round, and we’re never more than an email or phone call away. As always, everything's covered by our RIFT Guarantee. As long as you've given us complete and accurate information, your rebate is protected.

Find out more about the Construction Industry Scheme (CIS) and how to register if you need to.

When you file your own Self Assessment tax returns, it's easy to miss out on CIS claims or make costly mistakes. Under the CIS scheme, your employer takes tax directly from your pay before you get it. This almost always means you're instantly losing 20% to the taxman. As a result, you’ll probably find you’ve been overcharged by HMRC when you file your Self Assessment tax return.

It takes specialist understanding to claim tax back for CIS construction workers. Every year, far too many people are still shelling out tax they don't owe. In the worst-case scenario, they don’t get any CIS tax rebate at all. Even if they do, it’s often nowhere near as much as they deserve.

Yes! All self-employed people, including CIS workers, have to complete a yearly Self Assessment return. The tax year runs until on 5th April, then you've got until the following 31st of January to complete and file your tax return.

Find out more about the Construction Industry Scheme (CIS) and how to register if you need to.

Read our guide to CIS and Self-Assessment

With RIFT, filing and completing your CIS tax return is all part of our tax rebate service. Armed with a list of your workplaces for the year and a few more details, we'll work out the cost of your travel and what you’re owed for it. Next, we'll add any other essential expenses you’ve had and sort out your paperwork.

We'll send the forms to HMRC, handle any questions on your behalf and keep chasing the taxman until your rebate’s paid. 95% of our CIS customers get a tax refund, with an average value of over £1,705 per year.

The taxman really doesn’t like waiting. Miss the filing or payment deadline by a single day and you'll get an immediate £100 penalty. At 2 months late, that fine doubles. At 6 and 12 months late, it reaches £300 (or 5% of the CIS deductions on the return, if that's higher). Any longer and you might face an additional penalty of £3,000, or 100% of the CIS deductions on the return.

Of course, with RIFT on your team, you’ve got nothing to worry about. We’ll keep you in the taxman's good books and make sure you never miss out on your CIS tax claims - even the ones you didn’t know you qualified for!

Find out more about the Construction Industry Scheme (CIS) and how to register if you need to.

You’ll need a few bits of information about yourself to register for the Construction Industry Scheme:

The CIS scheme covers most of the construction work done in the UK. If you’re self-employed in the building trade, you’ll almost certainly have to register for it. Contractors will need to verify their subcontractors, handle their CIS deductions and file monthly CIS returns.

If you’re a subcontractor and don’t sign up for CIS, it doesn’t mean you won’t have the deductions taken from your pay. In fact, you’ll probably actually lose even more of your money, since the rate goes up to 30% for people who aren’t CIS-registered. It’s possible that you qualify for “gross payment” status, where you don’t have to pay CIS deductions. Don’t count on that, though, as there are specific rules and conditions to meet.

One of the problems with CIS is that it's very easy to end up paying too much - and you won't get an automatic refund. To claim your CIS rebate, HMRC demands proof of what you’re owed. This is what RIFT Tax Refunds is all about, so get in touch to see how we can help.

If you are currently working PAYE (on the books) and need to switch to CIS we can help you.

Remember that CIS covers all UK construction work, even if it's done by foreign firms. There are penalties for filing late, so you have to stay on top of the paperwork.

Find out more about the how to register for CIS if you need to.

When you register with the Construction Industry Scheme, you get a card. The kind you’re given depends on your situation:

Find out more about the Construction Industry Scheme (CIS) and how to register if you need to.

For most general contractors in the UK building trade, the CIS scheme's compulsory. It includes everything from site preparation and repairs to decoration and demolition. There are a few exceptions, though. For instance, if you’re a contractor who only deals with very limited sections of the work (like carpet fitting), you may not have to register.

Find out more about the how to register and who needs to.

CIS covers all construction work done in the UK, even when it's done by foreign firms. The registration system is a little different, but all the basic rules are the same. The UK has some ''double taxation'' agreements in place with various other countries to reduce your total tax when you're paying in both countries. Talk to RIFT if you need help working out what it all means for you.

Read our guide to CIS and Self Assessment

The standard Construction Industry Scheme tax deduction is 20%. If that sounds like HMRC's taking a huge lump out of your pay, then it only gets worse if you don’t sign up to the scheme. If you haven’t registered, the rate shoots up to 30%! This can also happen if you don't give your employer your Unique Taxpayer Reference number (UTR). Your UTR is used by HMRC to identify you. If your employers don't have it, the taxman might assume you aren't registered for CIS and charge you the higher rate.

Find out more about the Construction Industry Scheme (CIS) and how to register if you need to.

CIS tax deductions are payments your employer takes out of your wages before you get them. Those payments go straight to HMRC instead of you. They're supposed count as advance payments toward your tax and National Insurance, clamping down on tax evasion in the industry. Unfortunately, one of the side-effects of CIS is that a lot of honest people end up being charged too much tax. At RIFT, our friendly teams of CIS experts can quickly tell you if you're due a tax rebate, then make sure you get it.

Find out more about the Construction Industry Scheme (CIS) and how to register if you need to.

A Construction Industry Scheme Payment and Deduction statement is a record of the money you've been paid and taxed on if you work under the CIS scheme. You might also just call them wage slips, payslips or something similar.

If you're self-employed in construction, they're some of the most important documents you'll ever have. When you file your yearly CIS tax return, you'll need these statements to prove what you've earned and paid. You should get a CIS Payment and Deduction statement from your boss whenever you’re paid, within 14 days of the end of the tax month.

The main thing you'll need your CIS certificates or wage slips for is filing your yearly Self Assessment tax returns. The taxman will expect you to show him a record of all the cash you’ve got coming in. With the CIS taking 20% of your pay before you get it, you’re probably not getting the full benefit of your tax-free Personal Allowance. You’ll be hard-pressed to prove that without your CIS paperwork to back up your claim, though.

Find out more about the Construction Industry Scheme (CIS) and how to register if you need to.

Read our guide to CIS and Self-Assessment

Employment status is a huge issue in construction, and it can get very complicated with so many layers of contractors, subcontractors, agencies and so on. You might think you’re working under exactly the same conditions as your PAYE workmates, but the taxman could well take a different view.

The first thing to do is check your payslips. If they say “CIS statement” and show 20% deductions being made, then you’re being taxed through CIS. If that seems wrong, you need to talk to your employer fast.

The CIS scheme is only for construction, and its rules can catch out even experienced self-employed people from other industries. If you’ve got self-employed mates from outside of construction, be careful taking Self Assessment advice from them. They might not know the territory as well as they think they do. Play it safe and talk to the experts at RIFT instead.

In construction, a contractor is a person or business supplying materials or labour for a job. On the other hand, a subcontractor is anyone who does construction work for a contractor. Basically, according to HMRC, you're a contractor if you pay subcontractors for construction work.

You can also count as a construction contractor if your business doesn't do construction work, but still spends an average of over £1m a year on construction in any 3-year period. Either way, you’ll need to register for CIS and start taking deductions from your subcontractors’ pay.

Find out more about the Construction Industry Scheme (CIS) and how to register if you need to.

Start My Claim

As a contractor, you need to register for CIS before you even take on your first subcontractor. You're going to have a lot of responsibilities under the scheme, so get used to minding the details. Here's what you need to do:

Subcontractor tax refunds can be tricky. It’s easy to miss out on money you’re owed - or even get put off from claiming altogether. Even pricey accountants can find themselves tangled up in the system if they don't know the construction industry well. RIFT Tax Refunds has been specialising in construction rebates since 1999. There really are no safer hands to be in.

Gross payment status means that no CIS deductions get taken out of your pay. There are 3 basic tests to see if you qualify:

Yes, you will pay tax “at source” (your tax is taken off your wages before you get them), most likely at the rate of 20% of your income.

However, this doesn’t mean you are “employed”. You still count self-employed under CIS – even if it doesn’t feel like it. The big difference is that this means you'll still have to do Self Assessment each year. Not filing those tax returns each year brings three very serious problems your way:

If you're getting CIS statements and don't understand why, get in touch with RIFT straight away. We can explain the system, make sure you aren't paying too much tax and keep you out of trouble with HMRC.

Find out more about the Construction Industry Scheme (CIS) and how to register if you need to.

There are strict rules for CIS contractors about payment and deduction statements. They need to send you one every time you're paid, with specific deadlines to hit.

If you haven't been receiving yours, don't panic. It may just be a simple admin mix-up. Get in touch with your contractor and ask for your certificates, so you can keep your Self Assessment records up-to-date.

Don't just ignore the problem. If it turns out your contractor's not been doing things correctly with HMRC, things could get awkward for you in a hurry, come the end of the tax year.

You will need the statements to submit your tax return, read our guide to CIS and Self-Assessment

If you still have no luck, come to RIFT for advice and help. We're experts in sorting out tax problems for UK construction, and we'll get straight to work.

If you're self-employed in any kind of business, you'll almost certainly be using Self Assessment to pay your tax. In the construction industry, you'll probably also have to deal with the Construction Industry Scheme (CIS). Subcontracting under CIS means your Self Assessment filing has a couple of extra points to consider. If you don't understand the system, it's easy to end up paying a lot of extra tax you don't owe. If you think you are due a tax rebate check out our CIS tax refund pages.

Self-employed CIS workers can sometimes pass work on to other people. However, there are strict rules about doing this, and breaking them can lead to serious trouble. HMRC has a real problem with people in CIS work paying cash-in-hand for others to do jobs for them. It doesn't matter if you're passing the work on to friends, colleagues or family. You still have to follow the rules.

Read more about the Construction Industry Scheme (CIS) and how to register if you need to.

The first thing to know is that passing your CIS work on makes you a contractor in HMRC's eyes. That means you have to register yourself to avoid serious trouble from the taxman. You can't just slip someone a fistful of banknotes on the sly and sort things out later. You need get yourself registered before you take on your first subcontractor.

After that, you need to be sure your subcontractors are signed up for CIS. When you pay your subcontractors, you have to take CIS deductions from their pay and send them to the taxman. You'll also need to file returns every month and keep detailed CIS records. If you slip up, or ignore the regulations altogether, you're looking at some painful penalties.

Find out more about the Construction Industry Scheme (CIS) and how to register if you need to.

As long as you're following the rules, then the cash you're paying the people you give the work to counts as an expense. That means it will bring down the amount of profit you're paying tax on. If RIFT is handling your tax returns, of course, we'll handle all of this for you as part of the service.

If you've been passing some of your CIS work on, then you need to have good records to show the taxman. HMRC will expect to see detailed evidence of the wages you've paid out, for instance. In addition, they'll also want to see the details of the people doing the work for you. Names, addresses and their Unique Taxpayer Reference numbers will all be needed. Again, RIFT will handle all the sticky HMRC business for you to keep you within the regulations and out of trouble.

RIFT was first founded to help construction workers tackle the taxman. We've grown a lot since then, but we always remember where we started. We're still the leading experts on taking care of the UK's construction industry. We're on great terms with HMRC, and know the business inside and out. Whatever tax problems or questions you've got, talk to RIFT.

Read more about the Construction Industry Scheme (CIS) and how to register if you need to.

The first thing to understand about healthcare tax refunds is that not every mile you travel or pound you spend will count toward your claim. A daily commute to a permanent workplace, for example, won’t earn you any tax relief. To qualify for a refund, your work travel needs to be to and from what HMRC calls “temporary workplaces”. In practice, this generally means anywhere you work for less than 24 months. So, for example, a nursing job that requires you to travel out to patients’ homes could end up making you eligible for a pretty decent tax refund. Meanwhile, travel expenses can also include some subsistence costs while you're on the move. Things like accommodation and food can all contribute toward your claim.

There are also a few tricky points to consider. If you're travelling to a number of hospitals or clinics within the same general area, with your mileage and travel times not changing much, HMRC might consider the entire region your “permanent workplace”. It's always best to get professional advice in situations like these.

Rotational contracts, where you're working full-time at a series of hospitals over a period of years usually won't qualify. However, if your training takes place under, for example, a single 5-year contract, then things changes. In that case, each hospital you work at will count as temporary because it's a single employment with multiple temporary workplaces. The regulations are easy to trip over here, so it's often a good idea to get professional help.

If you're already getting some of your costs reimbursed by your employer, you may still be owed tax back. HMRC has set rates for Approved Mileage Allowance Payments (AMAP), and if you're not getting the full amount you can claim back the difference. The NHS has its own rates as well, if you're employed by them.

Beyond travel, there are several more ways a job in healthcare can cost you money. If you’re paying out of your own pocket for repair, replacement or even laundry of your work uniform, for instance, you could make a claim for those costs. The same goes for union dues and professional body fees to organisations like the Nursing and Midwifery Council.

The key points to remember are that the costs you’re claiming tax relief for need to be essential to your work, and you need to be paying them yourself. In addition, to get back everything you’re owed you’ll need to show proof of what you’re spending. That means records and receipts – although the simplified Flat Rate Expenses system can offer an easier way if you don’t mind sticking to HMRC’s figures.

If you find yourself buying things like laptops or office equipment for work use, you might have a claim under HMRC’s capital allowances system. This is generally for items that you’ll be using for a couple of years or more – and again, you’ll need to be footing the bill yourself for them to qualify for tax relief.

Your personal tax specialist will get to work on your refund.

As they prepare your claim they might need to ask you a question or two to make sure you get the most from your refund. They’ll always try to call first and if they can’t get through they’ll send you an email or text from 01233 628648 so save that number in your phone.

If there’s a particular time you’d prefer we try to contact you, just let us know.

We'll now send these to HMRC.

It takes HMRC, on average, approximately 12 weeks to process these forms and release your refund (times can vary). We'll make sure we chase them during this time.

As soon as HMRC release the refund we'll contact you to confirm sending you your money.

We'll keep you updated if HMRC take longer than anticipated.

In the meantime keep good records of your travel and refer your friends to us to earn additional money.

Our standard charges are:

When we receive your refund from HMRC we take out our fee and then pay it the refund to you. There are no up front charges to pay for anything. If you are not due a refund then there is no charge.

Before we send your claim to HMRC we sent a copy to you with a full breakdown of all the fees so you can clearly see:

You will need to sign and send this back to us to say you have read, understood and agreed with it, along with a declaration that all the information you have provided about your claim is true. This means you will never be charged any fees you have not agreed to.

There are no further fees to pay, and no hidden charges.

All aftercare is included (if you need us to call HMRC on your behalf, if you have a problem you would like us to resolve with them, if your tax code needs correcting etc).

Your refund is covered by the unique RIFT Guarantee which means that whatever happens, your refund stays in your own pocket and will never go back to HMRC. If we fight any HMRC enquiries for you (still included in the cost) and if anything did go wrong (which it never has in 15 years) we would pay back the refund to HMRC ourselves.

We will also send you a reminder when it's time to see if you have a claim next year.

Does it apply to me?

The short answer is "yes".

While many people get their travel and work expenses reimbursed by their employers those in the Armed Forces, Construction Trades, Security and Offshore industries often don't.

To get the money back you have to put in a claim to HMRC to show what you've spent so they know how much to pay you back.

Sadly many people, 2 in 3, who are owed tax refunds don't claim them back - meaning they are losing a chunk of their wages.

It's our mission to improve knowledge about this so that all workers who should be claiming are claiming.

We know what it's like - time flies and it's hard to find a moment to get round to things.

The good news is, we take care of everything for you - the whole reason we do what we do is to take the stress off your hands and give you time back as well that hard earned cash.

All it takes is 10 mins on the phone or chat to get an average of £2,500 refunded. That's got to be the most valuable time you could spend on your phone today.

Once we've got your info we do all the chasing, calculations, sorting out the payments - and that's before we even get to our all inclusive aftercare!

Yes - absolutely! If you've paid too much tax, you're fully entitled to a tax rebate.

Travel and mileage tax refunds for travel to temporary workplaces are claimed under Income Tax (Earnings and Pensions) Act 2003, sections 336-339.

There's over 1000 pages of rules and regulations but our experts will get it sorted for you. They have qualifications from the Association of Tax Technicians, Associations of Accounting Technicians, and The Association of Chartered Accountants. Having these qualifications mean they are bound by all its rules, regulations, ethics and codes of conduct in addition to our internal standards.

HMRC can't issue automatic refunds for Work and travel expenses because it's not based on information they have - like your salary or tax code. You have to prove what you've spent and claim what you're owed, which puts far too many people off getting back their own cash.

I'm not sure I have the info?

To make your claim the key things we need to know are:

We have access to a number of specialised custom built systems that link to HMRC, Government depts, DVLA, travel routes, etc and can get the information for you.

I don't know anyone who's done it.

You're absolutely right to be cautious. There's a lot of scams to be aware of and a word of mouth recommendation from someone you trust is the best way to be sure.

We don't know who your friends are, but if they're in the Armed Forces, Construction Trades, Security or Offshore ask them if they've used us. 97% say they would recommend us.

A lot of people have - we've helped 130,000 customers make claims in the last 20 years - but British people don't really talk about money so it's not something that tends to come up in conversation.

Otherwise, check us out on Trust Pilot. It's the next best thing.

First we need to talk to you on the phone or online run through some questions about your work and travel and tell you how a claim is made.

If you would like to claim for you we send you a form to sign that lets us talk to HMRC on your behalf to do that.

We'll then give you your own Personal Tax Specialist who will gather all the information needed to calculate exactly what you're owed.

We send you the total to approve the amount and what our fee comes to and then submit it to HMRC for you.

You don't pay any fees upfront. To make it simpler for you we take the fee from the refund total and then pay it into your bank account.

It takes a few weeks to put together a really comprehensive tax refund claim. As soon as you're happy to go forward, we'll send your claim to HMRC for approval. It can take 8-10 weeks for the taxman to check your details and confirm your refund total, so the sooner you get us the information we need the sooner you'll have your money.

The best way to speed up your RIFT Tax Refund is to get your Authorising your agent (64-8) form back to us fast. This is the form that lets us tackle the taxman on your behalf. Without 2 physical copies of your 64-8 document, HMRC won't even speak to us about your claim. It's annoying, but it's all about protecting you.

As soon as your refund's paid out, we'll either send you a cheque or pay it into your bank account if you prefer. The choice is yours.

Have a look at our 'How Long Does A Tax Refund Take' page for more information about how long it takes to get your tax refund done and some pointers for how to make things happen as fast as possible.

Remember that you can claim for the last 4 tax years and you can make your claim at any time.

Please do!

Not only will you be doing them a big favour if you can get some cash back in their pockets but we'll pay you a £50 referral reward for anyone who does go on to claim through us.

Until the 9th of October we'll also pay you an extra bonus of £150 if 5 people claim with us (T&Cs apply)

If you tell them to apply now they'll get their tax refund in time for Christmas and you'll get something extra to stuff in your stocking. That could be £400 in your pocket as well as the warm glow you get from helping out your mates.

To get started:

Not sure which friends could claim? Find out more about who can claim tax refunds.

There's no limit to the number of people you can refer and we pay out the rewards every week. It could be a nice little extra in your pocket, as well as the lovely warm feeling you get from knowing you helped out a mate.

Find out more about the referral scheme.

In HMRC's language, a tax rebate is "a refund on taxes when the tax liability is less than the taxes paid". What it's definitely not is a prize or a dodgy way of ''cheating the system''. When you're owed a HMRC tax refund, it's because you've already paid too much tax.

When you're paying your own way to temporary workplaces, the odds are good that you're owed some tax back for your expenses. ''Temporary'' here just means it's somewhere you're working for less than 24 months on the trot. It's worth making sure you get back what you're owed, too. You can claim a tax rebate for up to 4 years, with an average 4-year rebate with RIFT coming to £3,000. This is based on average total claims data for a 4-year period. Refunds are subject to fees of 36%. Exclusions apply.

A lot of the time, people don't even realise how many of their day-to-day expenses qualify for tax relief. Unless you prove to HMRC what you're owed, though, the taxman won't have the information he needs to settle up. The tax rebate system's a little clunky in places, but RIFT's on-demand, 1-on-1 service means you'll never get lost or lose out.

Just answer a few simple questions and we can tell you whether it looks like the expenses you've had to pay out in the course of your work meant that you may have paid more tax than you should.

You can also use our tax refund calculator to see an estimate of how much you could be due if you make a claim.

Our standard charges are:

Don't worry if you had a mixture of self-employed and PAYE (employed by a company) work during the period you want to claim for. We can work out if you would be due a refund and let you know what the fee would be.

See our full list of services with prices and options.

When we receive your refund from HMRC we take out our fee and then pay you your refund. There are no up front charges to pay for anything. If you are not due a refund then there is no charge.

Before we send your claim to HMRC we send a copy to you with a full breakdown of all the fees so you can clearly see:

You will need to sign and send this back to us to say you have read, understood and agreed with it, along with a declaration that all the information you have provided about your claim is true. This means you will never be charged any fees you have not agreed to.

There are no further fees to pay, and no hidden charges.

All aftercare is included (if you need us to call HMRC on your behalf, if you have a problem you would like us to resolve with them, if your tax code needs correcting etc).

Your refund is covered by the unique RIFT Guarantee which means that whatever happens, your refund stays in your own pocket and will never go back to HMRC. If we fight any HMRC enquiries for you (which is included free of charge) and if they did demand any money back, we would pay back the refund to HMRC ourselves.

We will also send you a reminder when it's time to see if you have a claim next year.

If you don't have a P60 we you can use your last payslip or income statement. We can also get copies of the P60 directly from HMRC.

Visit our checklist for details of the documents you need and what to do if you are missing anything.

You can reach us on the phone or Livechat

You can email us or send us a question or feedback through our contact page at any time and you can leave us a private message through our Facebook page.

A tax return is a form you use to tell HMRC about your earnings and expenses. It's a complete overview of the taxable income you've made and the costs of doing business you've faced.

A tax refund is money HMRC gives back when you've paid too much tax. There are several reasons why you might overpay, and you often have to file a claim and prove you did.

There’s basically no acceptable excuse for missing self assessment tax return deadlines, even if you don't owe HMRC anything. If you miss the deadline there are a number of self assessment tax return penalties that you could be hit with:

We’re here to take care of everything - from completing your tax return, through calculating any refunds due, to speaking to HMRC on your behalf. You can also get more self assessment tax return tips and advice here with some clear ''dos'' and ''dont's''.

Find out more about self assessment deadlines and penalties.

When you're claiming tax relief for food, you need to keep hold of things like receipts and order tickets as evidence of what you’ve spent. If you're paying by card, keep the slip that comes out of the machine. You can also get this information from bank statements but that will be much harder work.

If you take cash out of a machine to pay then take a quick photo of the withdrawal receipt. However, as with your bank statement this will only show what you took out, not what you spent so get a photo of the till total or anything else that shows the actual price you paid.

It’s a good idea to take a photo the price board or menu as extra evidence of your claim. If the menu doesn’t change you don’t have to take the same picture everyday – just one to show the prices is fine.

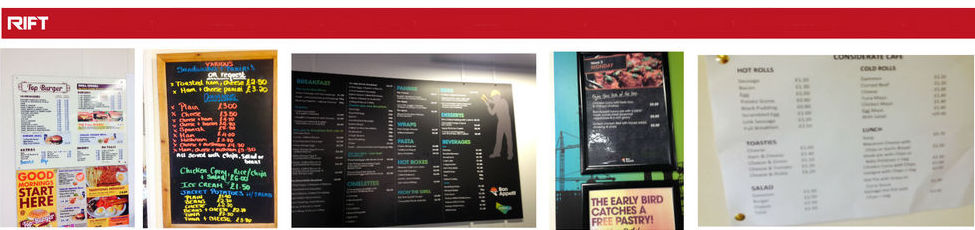

Here are some examples that customers have taken in the past. You don't need to take an award winning photo, just a quick snap of the prices like this will do.

You won’t need us to send all the records for us to do your claim but we need to know that you have evidence of your spending in case HMRC do ask for it and to make sure you're protected by our RIFT Guarantee.

We can make a refund claim for your food related expenses as part of your travel tax refund, but not as a stand alone expenses claim.

You don’t need to keep lots of paper. Store any photos, screenshots or scans somewhere you can easily find them on your computer. For now, just hold onto them. We may need to ask you for these at a later date to support your claim.

It's a good idea to take a photo of the menu board or price list where you bought your food. If it doesn’t change, you don’t have to take the same picture everyday – just one to show the prices like these ones taken at real works canteens.

If you order your food online then save the confirmation email.

You probably won't need them all to back up your tax refund claim but we need to know that you have the evidence if the tax man does ask for it.

We can make a refund claim for your food related expenses as part of your travel tax refund, but not as a stand alone expenses claim.

It's tricky to claim tax relief if you don't have proof of what you've spent. We may still be able to include your food costs in your refund claim if you’re working on a site where we have details of standard costs for.

Just remember to start keeping your records from now on to make things easier next year.

Use our tax calculator to find out if you're due a refund.

Yes. If you are staying overnight for work and your employer does not refund the money you spent on meals then you can claim tax relief in the same way as you can with other work related expenses.

Again, it’s important that you’re honest. Don’t claim to have eaten a 3 course meal in the hotel restaurant if you popped out to the local takeaway.

Don't forget to claim for the cost of food purchased during travelling to your temporary workplace. Whether you buy your food from the buffet trolley, the service station or at a shop or takeaway en route remember to keep the evidence so that we can claim the tax relief for you.

If you can't get a receipt for your food, even a photo of the price board can be helpful in proving what you've spent. Just take a quick snap with your phone and keep it safe. The taxman's not trying to trip you up or cheat you out of money. All he's after is evidence to back up your claim, so he's sure you're paying the right amount of tax.

You won’t need to send us all the photos for your claim. We just need to know you have them in case HMRC do ask for some evidence of your costs to make sure you're covered by the RIFT Guarantee.

Sometimes but if the subsistence allowance completely covers the cost of your food while you’re away from home for overnight stays then you can’t claim anything else.

If the amount does not cover all your expenses for food then you will be able to claim the difference.

If you’ve made your lunch at home, then you can’t claim the costs. This is because the groceries are part of your personal shopping bill, not work related expenses.

It's often strange little details like this that easily trip people up. That's why we're here to help make sure you get the best refund possible and always stay on the right side of HMRC's rules.

Use our Tax Calculator to find out if you can claim.

If you’re self-employed, freelance, contracting or working CIS in construction, this will be handled under your expenses in your self-assessment tax return in the normal way.

The same principles apply though, you will need to be able to provide evidence of what you’ve spent in order to claim them as costs. Keep your meal receipts in the same way as you keep all your other records needed for your tax return.

You can still claim even if your canteen is subsidised - but only for the subsidised amount that you paid.

Make sure to keep a record of what you spend so that we can work out the total at the end of the year.

If you didn’t get a receipt or meal ticket then just take a photo of the menu board or price list where you bought your food. If it doesn’t change, you don’t have to take the same picture everyday – just one to show the prices is fine.

Many people assume it’s not worth the hassle of keeping records of what you spend on meals because the refund you get back won’t be worth it.

Shockingly it turns out that you're probably looking at about a staggering £90,000 spent on food over your working life – that’s enough to pay off an average mortgage 6 years early!

The cost of food varies a lot up and down the country, and depends on things like whether you have a subsidised canteen at work. Still, the average daily spend of a person at work is £5 - £10. This means you should be getting £250 - £480 more back from HMRC in your refund every year.

If you don’t claim you’re missing out, on average, around £12-25k over the course of your working life – and that’s a considerable amount of money for taking a few photos of what you had for lunch.

Let's have a look at some examples:

Bill, is a builder working on a construction site in London.

Were you keeping track? Bill’s spent £9.94 already – and he’s probably a bit dehydrated at that!

All pretty simple so far, right? Only, Bill had to trek down from his home in Scotland for this job and travel home at weekends. He claims his tax refunds for the food he buys during his work day, but he's still missing out badly.

This means he spends £22.25 on food during his travels to work.

We can make a refund claim for your food related expenses as part of your travel tax refund, but not as a stand alone expenses claim.

Use our Tax Refund Calculator to find out what you could claim.

If you’re travelling to a temporary workplace then you can claim the costs for food purchased during this time.

This might be when you are travelling during the working day to temporary workplaces or it might be if you have to travel a long distance to get to a temporary site that you’re staying over at.

Whether you buy your food from the buffet trolley, the service station or at a shop or takeaway en route remember to keep the evidence so that we can claim the tax relief for you.

Find out what you could claim with our Tax Calculator.

If you’re part of the Hungry Soldier scheme then you sign for your meals and the cost is taken directly out of your salary in arrears. You will need to keep a record of how much this adds up to each month and let us know what you spent.

The amount taken out should be shown on your payslip. You’ll need to give us copies of your payslips for your travel refund anyway, so you should be keeping those.

Use our Tax Refund Calculator to find out how much you could claim.

When you're claiming tax relief for food, you need to keep hold of things like receipts and order tickets as evidence of what you’ve spent. If you're paying by card, keep the slip that comes out of the machine. You can also get this information from bank statements but that will be much harder work.

If you take cash out of a machine to pay then take a quick photo of the withdrawal receipt. However, as with your bank statement this will only show what you took out, not what you spent so get a photo of the till total or anything else that shows the actual price you paid.

It’s also a good idea to take a photo of the price board or menu as extra evidence of your claim. If the menu doesn’t change you don’t have to take the same picture everyday – just one to show the prices is fine.

If you haven’t been good at keeping receipts to date, start keeping them from now on to make claiming easier next year. You wouldn’t throw away a £5 note, so don’t throw away your receipts as that’s what they could be worth to you.

We can make a refund claim for your food related expenses as part of your travel tax refund, but not as a stand alone expenses claim.

Use our Tax Refund calculator to find out how much you can claim.

You don’t need to keep lots of paper. You can take photos or scans of them and save them somewhere you can easily find them on your computer.

For now, just hold onto them. We may need to ask you for them at a later date to support your claim.

You may not need to send them to us for your tax refund claim but we need to know that you have the evidence to hand if HMRC does ask for it so that you're protected by the RIFT Guarantee.

This depends on quite a few factors about your personal situation, so it’s best to speak to us directly and we’ll talk it through with you and let you know what to do.

You can claim for your meals bought in the Cookhouse or Mess during working hours though.

Read more about tax refunds for the Armed Forces.

This depends on whether your permanent residence is elsewhere. If you’re not sure and want to talk it through with us then give us a call and we’ll let you know how the rules apply to your situation.

If it is then you can claim tax relief against the costs of any takeaways or meals out you have to buy.

If you ordered online keep a copy of the email confirmation or save a screenshot.

If you went to the takeaway, then take a photo of your receipt or the menu board.

Use our Tax Calculator and find out if you're due a refund.

If you’re in Substitute Living Single Accommodation (SSA), you’ll get an additional allowance given to purchase food as you won’t be entitled to use the Cookhouse. You get this as a supplement in your pay so you can only claim if your expenses exceed the amount of the allowance.

Find out more about tax refunds for members of the Armed Forces.

Food that you don't personally pay for can't be claimed against for tax relief. For example, if you're at sea in the Royal Navy, your meals are provided for you and don't count toward you tax refund.

You should keep track of any meals you have to buy onshore or off-base, though, as those can often count.

Read more about tax refunds for the Armed Forces.

If you’re part of the Hungry Soldier scheme then you sign for your meals and the cost is taken directly out of your salary in arrears. You will need to keep a record of how much this adds up to each month and let us know what you spent.

The amount taken out should be shown on your payslip. You’ll need to give us copies of your payslips for your travel refund anyway, so you should be keeping those.

Use our Tax Refund Calculator to find out how much you could claim.

When you're claiming tax relief for food, you need to keep hold of things like receipts and order tickets as evidence of what you’ve spent. If you're paying by card, keep the slip that comes out of the machine. You can also get this information from bank statements but that will be much harder work.

If you take cash out of a machine to pay then take a quick photo of the withdrawal receipt. However, as with your bank statement this will only show what you took out, not what you spent so get a photo of the till total or anything else that shows the actual price you paid.

It’s also a good idea to take a photo of the price board or menu as extra evidence of your claim. If the menu doesn’t change you don’t have to take the same picture everyday – just one to show the prices is fine.

If you haven’t been good at keeping receipts to date, start keeping them from now on to make claiming easier next year. You wouldn’t throw away a £5 note, so don’t throw away your receipts as that’s what they could be worth to you.

We can make a refund claim for your food related expenses as part of your travel tax refund, but not as a stand alone expenses claim.

Use our Tax Refund calculator to find out how much you can claim.

You don’t need to keep lots of paper. You can take photos or scans of them and save them somewhere you can easily find them on your computer.

For now, just hold onto them. We may need to ask you for them at a later date to support your claim.

You may not need to send them to us for your tax refund claim but we need to know that you have the evidence to hand if HMRC does ask for it so that you're protected by the RIFT Guarantee.

This depends on quite a few factors about your personal situation, so it’s best to speak to us directly and we’ll talk it through with you and let you know what to do.

You can claim for your meals bought in the Cookhouse or Mess during working hours though.

Read more about tax refunds for the Armed Forces.

This depends on whether your permanent residence is elsewhere. If you’re not sure and want to talk it through with us then give us a call and we’ll let you know how the rules apply to your situation.

If it is then you can claim tax relief against the costs of any takeaways or meals out you have to buy.

If you ordered online keep a copy of the email confirmation or save a screenshot.

If you went to the takeaway, then take a photo of your receipt or the menu board.

Use our Tax Calculator and find out if you're due a refund.

If you’re in Substitute Living Single Accommodation (SSA), you’ll get an additional allowance given to purchase food as you won’t be entitled to use the Cookhouse. You get this as a supplement in your pay so you can only claim if your expenses exceed the amount of the allowance.

Find out more about tax refunds for members of the Armed Forces.

Food that you don't personally pay for can't be claimed against for tax relief. For example, if you're at sea in the Royal Navy, your meals are provided for you and don't count toward you tax refund.

You should keep track of any meals you have to buy onshore or off-base, though, as those can often count.

Read more about tax refunds for the Armed Forces.

When you're claiming tax relief for food, you need to keep hold of things like receipts and order tickets as evidence of what you’ve spent. If you're paying by card, keep the slip that comes out of the machine. You can also get this information from bank statements but that will be much harder work.

If you take cash out of a machine to pay then take a quick photo of the withdrawal receipt. However, as with your bank statement this will only show what you took out, not what you spent so get a photo of the till total or anything else that shows the actual price you paid.

It’s a good idea to take a photo the price board or menu as extra evidence of your claim. If the menu doesn’t change you don’t have to take the same picture everyday – just one to show the prices is fine.

Here are some examples that customers have taken in the past. You don't need to take an award winning photo, just a quick snap of the prices like this will do.

You won’t need us to send all the records for us to do your claim but we need to know that you have evidence of your spending in case HMRC do ask for it and to make sure you're protected by our RIFT Guarantee.

We can make a refund claim for your food related expenses as part of your travel tax refund, but not as a stand alone expenses claim.

You don’t need to keep lots of paper. Store any photos, screenshots or scans somewhere you can easily find them on your computer. For now, just hold onto them. We may need to ask you for these at a later date to support your claim.

It's a good idea to take a photo of the menu board or price list where you bought your food. If it doesn’t change, you don’t have to take the same picture everyday – just one to show the prices like these ones taken at real works canteens.

If you order your food online then save the confirmation email.

You probably won't need them all to back up your tax refund claim but we need to know that you have the evidence if the tax man does ask for it.

We can make a refund claim for your food related expenses as part of your travel tax refund, but not as a stand alone expenses claim.

It's tricky to claim tax relief if you don't have proof of what you've spent. We may still be able to include your food costs in your refund claim if you’re working on a site where we have details of standard costs for.

Just remember to start keeping your records from now on to make things easier next year.

Use our tax calculator to find out if you're due a refund.

Yes. If you are staying overnight for work and your employer does not refund the money you spent on meals then you can claim tax relief in the same way as you can with other work related expenses.

Again, it’s important that you’re honest. Don’t claim to have eaten a 3 course meal in the hotel restaurant if you popped out to the local takeaway.

Don't forget to claim for the cost of food purchased during travelling to your temporary workplace. Whether you buy your food from the buffet trolley, the service station or at a shop or takeaway en route remember to keep the evidence so that we can claim the tax relief for you.

If you can't get a receipt for your food, even a photo of the price board can be helpful in proving what you've spent. Just take a quick snap with your phone and keep it safe. The taxman's not trying to trip you up or cheat you out of money. All he's after is evidence to back up your claim, so he's sure you're paying the right amount of tax.

You won’t need to send us all the photos for your claim. We just need to know you have them in case HMRC do ask for some evidence of your costs to make sure you're covered by the RIFT Guarantee.

Sometimes but if the subsistence allowance completely covers the cost of your food while you’re away from home for overnight stays then you can’t claim anything else.

If the amount does not cover all your expenses for food then you will be able to claim the difference.

If you’ve made your lunch at home, then you can’t claim the costs. This is because the groceries are part of your personal shopping bill, not work related expenses.

It's often strange little details like this that easily trip people up. That's why we're here to help make sure you get the best refund possible and always stay on the right side of HMRC's rules.

Use our Tax Calculator to find out if you can claim.

You can still claim even if your canteen is subsidised - but only for the subsidised amount that you paid.

Make sure to keep a record of what you spend so that we can work out the total at the end of the year.

If you didn’t get a receipt or meal ticket then just take a photo of the menu board or price list where you bought your food. If it doesn’t change, you don’t have to take the same picture everyday – just one to show the prices is fine.

Many people assume it’s not worth the hassle of keeping records of what you spend on meals because the refund you get back won’t be worth it.

Shockingly it turns out that you're probably looking at about a staggering £90,000 spent on food over your working life – that’s enough to pay off an average mortgage 6 years early!

The cost of food varies a lot up and down the country, and depends on things like whether you have a subsidised canteen at work. Still, the average daily spend of a person at work is £5 - £10. This means you should be getting £250 - £480 more back from HMRC in your refund every year.

If you don’t claim you’re missing out, on average, around £12-25k over the course of your working life – and that’s a considerable amount of money for taking a few photos of what you had for lunch.

Let's have a look at some examples:

Bill, is a builder working on a construction site in London.

Were you keeping track? Bill’s spent £9.94 already – and he’s probably a bit dehydrated at that!

All pretty simple so far, right? Only, Bill had to trek down from his home in Scotland for this job and travel home at weekends. He claims his tax refunds for the food he buys during his work day, but he's still missing out badly.

This means he spends £22.25 on food during his travels to work.

We can make a refund claim for your food related expenses as part of your travel tax refund, but not as a stand alone expenses claim.

Use our Tax Refund Calculator to find out what you could claim.

If you’re travelling to a temporary workplace then you can claim the costs for food purchased during this time.

This might be when you are travelling during the working day to temporary workplaces or it might be if you have to travel a long distance to get to a temporary site that you’re staying over at.

Whether you buy your food from the buffet trolley, the service station or at a shop or takeaway en route remember to keep the evidence so that we can claim the tax relief for you.

Find out what you could claim with our Tax Calculator.

Yes, as well as your 4 quarterly updates, a final tax return (also called a Final Declaration) will still need to be submitted by the following 31st January.

The final declaration

After the tax year ends (5 April), you have until 31 January of the following year to submit a final declaration.

This is where you:

Think of quarterly updates as progress reports and the final declaration as your official statement.

No, it only changes how and when you report your income.

There are no changes to making payment.

Yes, for Self Employed and income from property of more that £50,000. Those above £30,000 will be included from April 2027.

Yes gross income (or turnover) is before any deductions such as expenses. The qualifying income thresholds would apply to your share if income from jointly owned property.

You’ll need to keep digital records for all of them and we’ll send updates for each income stream separately.

HMRC can issue fines or penalties for missed submissions.

MTD has introduced a points-based penalty system for late submissions and financial penalties for late payment.

Late submission penalties:

How points accumulate:

Points reset:

If you submit all your required updates on time for a full compliance period (usually 24 months), your points reset to zero.

Late payment penalties:

Example scenario:

How to avoid penalties:

Partnerships are not currently in scope of MTD.

Yes. Income from self employment, UK property and foreign property are in scope of MTD. It is gross income from self employment and rental income.

Not until April 2027

Not yet. Currently it is planned that this group will be included from April 2028.

Qualifying income is that from self employment and income from property. PAYE would not be considered in the qualifying income threshold test.

We’ll manage this for you. You’ll need to keep digital records for Income Tax if all of the following apply:

Under MTD for Income Tax, you'll submit quarterly updates instead of one annual tax return.

The quarterly cycle:

Each tax year is divided into four quarters:

In your quarterly update you must report on:

These are summary updates—you're reporting the figures calculated by your MTD-compatible software based on the digital records you've kept.

For construction industry workers, understanding how MTD interacts with the Construction Industry Scheme is crucial.

CIS deductions still apply:

MTD doesn't replace CIS. If you're a subcontractor, contractors will still deduct tax from your payments at 20% or 30% (or 0% if you have gross payment status). These deductions continue exactly as before.

Quarterly updates include CIS information:

When you submit your quarterly MTD updates, you'll report your construction income and the CIS tax that's been deducted. Your MTD-compatible software should help you track these deductions throughout each quarter.

CIS deductions count toward your tax bill:

The tax already deducted under CIS is credited against your total tax liability. At the end of the tax year, HMRC calculates your final tax bill and offsets the CIS deductions. If too much was deducted, you receive a refund. If too little, you pay the difference.

Example scenario:

Imagine you're a self-employed electrician. In quarter one, you earn £15,000 from construction work, with £3,000 deducted under CIS (20%). When you submit your MTD quarterly update, you report the £15,000 income and note the £3,000 already paid. Your software calculates whether you're on track for a refund or additional payment at year-end.

Importance of accurate contractor statements:

You need the monthly payment and deduction statements from your contractors to complete your MTD updates accurately. Keep these statements organised and check them against your own records.

While MTD requires significant changes, it offers several advantages for construction workers and contractors:

Real-time tax visibility:

Instead of waiting until the end of the tax year to discover your tax bill, MTD gives you a clearer picture throughout the year. You'll know approximately what you owe each quarter, helping you plan and budget more effectively.

Reduced errors:

Digital record-keeping and automatic calculations significantly reduce mathematical errors and missed deductions. MTD-compatible software can automatically categorise expenses and calculate allowances, reducing the risk of underpaying or overpaying tax.

Better cash flow management:

Quarterly updates help you spread your tax planning across the year. You can set aside money gradually rather than facing a large unexpected bill. For construction workers managing irregular income and CIS deductions, this visibility is particularly valuable.

Integration with CIS:

MTD software can integrate CIS deductions directly into your tax calculations. The tax already deducted under CIS is automatically accounted for, giving you a clearer view of whether you'll receive a refund or owe additional tax.

Time savings in the long run:

While there's an initial learning curve, digital record-keeping can save time compared to managing paper receipts and manual bookkeeping. Many MTD-compatible apps allow you to photograph receipts, track mileage, and categorise expenses on the go.

Improved compliance:

Regular quarterly submissions mean you're less likely to miss deadlines or forget important deductions. The software prompts you to submit updates, reducing the risk of penalties.

To comply with MTD, you must use software that meets HMRC's standards.

What makes software MTD-compatible:

You cannot:

Features to look for (construction-specific):

Finding compatible software:

HMRC maintains a list of MTD-compatible software providers on GOV.UK. You can filter by type of tax (Income Tax, VAT), business size, and features needed.

If you are a RIFT customer your subscription will include access to software as part of the service.

If you are a RIFT customer your subscription will include access to software as part of the service.

If you choose to do your own submissions HMRC has estimated that the initial cost to purchase the software will be around £320 and then £110 per year on an ongoing basis.

Some estimates have put the total investment required at four times that cost.

You'll need a MyRIFT account to hold all the information needed to make your tax refund claim with us. It's free to set up and it's the easiest way to update your info, track your documents and make your claim.

New to RIFT

If you're new to RIFT and wanting to get your claim started, have checked that you're due a refund by answering the 4 simple questions, and filled in your name, email address and created a password then you've already created your account. You should also have received a Welcome to RIFT email that contains more information about what happens next and has all the links you need.

Login page to continue updating your information.

If you need to reset your password, you can do that from the login page.

If you need any help, give us a call on 01233 628648 or use the Live Chat to talk to one of our Customer Service Team.

Returning to RIFT

If you've claimed with us before using a paper Refund Pack or Forms by Phone and not yet set up your MyRIFT account then get in touch by calling 01233 628648 or using the Live Chat below and we can get your account created and make it easier for you to claim this year.

Once you're logged in you'll be able to fill in your personal details, work locations, expense details and upload relevant documents. It's everything you're used to doing when making a claim with RIFT, but much quicker and easier now. You can also track the progress of your claim whenever, and wherever, you want to.

Once you are happy you have uploaded all the necessary information, press submit and we will take it from there!

You can call or Live Chat with us us 8.30am to 8.30pm Monday to Friday and 9.30am to 1.30pm Saturday.

Outside of these time you can send us an email to info@riftrefunds.co.uk or go to our Facebook page and send us a private message

If you're already a RIFT customer and have given us information online before then you'll have done that using your MyRIFT account. If you can remember your login details, you can sign, update your info for this year, upload your documents and get started right away.

It might be a year or more since you last used your MyRIFT account, so if you can't remember the details (email and password) you used to set it up just get in touch using the Live Chat here on the site, call 01233 628648 or drop us an email to info@riftrefund.co.uk and we'll get it all reset and ready for you to use again.

If you've claimed with us before using a paper Refund Pack or Forms by Phone and not yet set up your MyRIFT account then get in touch and we can get your account created and make it easier for you to claim this year.

If you're not sure if you've got an account get in touch and we can check for you. If you have, we'll help you get started, if not, we'll get you set up.

You can call or Live Chat with us us 8.30am to 8.30pm Monday to Friday and 9.30am to 1.30pm Saturday.

Outside of these time you can send us an email to info@riftrefunds.co.uk or go to our Facebook page and send us a private message

If you forget your password for your MyRIFT account, look below the log in button and you'll see a helpful link to ‘reset your password’.

Click the link, enter the email address you use to login to your MyRIFT account and we will email you a link to reset your password.

Once you get the email, open it and click the link which will take you a page where you'll be asked to create, and then confirm, the new password you want.

Press ‘change password’ and you will be taken to the homepage of your MyRIFT account.

If you can't remember the email address you used when setting up your account, or need help with anything else, please give us a call on 01233 628648 or use the Live Chat below and we can get you all set up.

If your email address has changed since you set up your account, or if you want to use a different email address for any reason then it's easy to update.

If you still have access to your old email account, use it to login and then you'll be able to update your email address on your MyRIFT Personal Dashboard.

If you no longer have access to your old email address, or can't remember it, and need us to update your account to your new address then give us a call on 01233 628648 or use Live Chat and our team will be happy to get it all sorted out for you.

There are a couple of reasons that you may have a MyRIFT account and not realise it.

Account created a long time ago

The most common is that you set one up when you first made an enquiry to RIFT, and that could have been quite a while ago. If you answered the 4 questions on our website to see if you were due a refund you would have been given the option to set up your account. Do you remember filling in your name, email address and creating a password? If so that's when it was set up and you would have also received a confirmation email.

If you have an account already, and can remember the details you gave when it was created, you can use them to login, reset your password or update your email, and then continue with your claim online.

If you aren't sure of any of the details you used and need us to reset them, give us a call on 01233 628648 or use Live Chat and our Customer Service Team can help you.

Account created for you by Customer Services and never needed

If you made a claim with us over the phone one of our Customer Service Team may have asked you if you would like them to set an account up for you to use. If they did this then you would have been sent an email with instructions on how complete the set up and create your password and confirm login details, but if this was it the case it was probably more than a year ago now.

What this means is that the account is sitting there in the system, even if you never needed to use it.

It's easy to get it reactivated so that you can update your info, upload your documents and track the progress of your claim this year, though.If you do still have the set up email, you can follow the instructions but it's probably easier to just give us a quick call on 01233 628648 or use Live Chat and we can get it all working for you.

You can call or Live Chat with us us 8.30am to 8.30pm Monday to Friday and 9.30am to 1.30pm Saturday.

Outside of these time you can send us an email to info@riftrefunds.co.uk or go to our Facebook page and send us a private message

If you're having trouble logging in and need to check the email address you used to set up your account, simply give us a quick call on 01233 628648 or use the Live Chat and our we'll be able to quickly check for you.

Once you know, you can log in and carry on, or if you'd like to update the email on the account then we can do that for you there and then.

You can call or Live Chat with us us 8.30am to 8.30pm Monday to Friday and 9.30am to 1.30pm Saturday.